Differential costs are the increase or decrease in total costs that result from producing additional or fewer units or from the adoption of an alternative course of action. The primary purpose of conducting a differential analysis is decision-making. So, we consider only relevant costs affecting the decision variables. Semi-variable expenses blend features of both fixed and variable costs.

Differential Cost in Pricing Strategies

They receive a special order for producing Mugs of 1000 units at a rate of ₹ 5/- per unit. Say one gadget costs more upfront but has lower operating expenses than its cheaper counterpart, with higher ongoing costs. The right pick could well be the pricier initial investment since it saves money in the long run.

Full Disclosure Principle in Modern Accounting Practices

Understanding fixed costs is essential for any accounting professional. They form an integral part of direct costs and indirect overheads in financial statements. Businesses must cover these ongoing expenses to keep their operations running smoothly. Opportunity cost refers to potential benefits or incomes that are foregone by choosing one option over another.

Are there different types of differential costs?

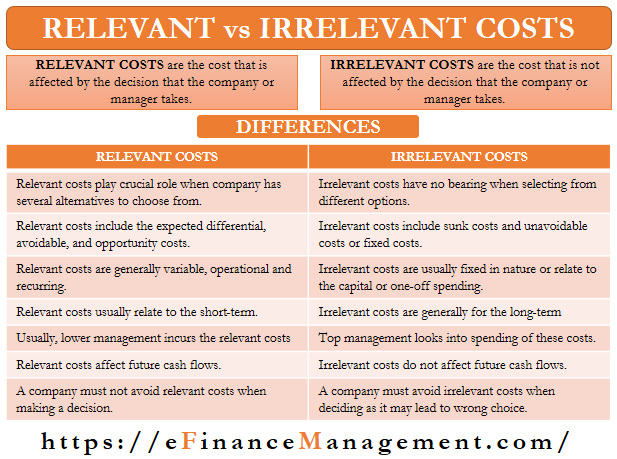

Therefore, all variable costs are not part of the differential cost and are considered only on a case-to-case basis. One of the primary components in differential cost analysis is the identification of relevant costs. These are costs that will be directly affected by the decision at hand.

- However, opportunity cost isa relevant cost in many decisions because it represents a realsacrifice when one alternative is chosen instead of another.

- The new regulation renders the machine and the produced plastic bags obsolete, and the company cannot change the government’s decision.

- Differential cost analysis helps managers choose between options.

- Understanding variable expenses helps managers choose the most cost-effective options.

- Differential costing involves the study of difference in costs between two alternatives and hence it is the study of these differences, and not the absolute items of cost, which is important.

- Suppose, present cost is Rs. 2,50,000 when the work is done by labour and the expected cost Rs. 2,25,000 when the work is done by machinery.

Our blog dives into the nuts and bolts of differential costs, helping you distinguish between variable, fixed, and semi-variable expenses. With real-life examples and clear explanations on types and analysis methods, we’ll guide you through using this powerful tool for sharper decision-making. Differential cost is the same as incremental cost and marginal cost. The difference in revenues resulting from two decisions is called differential revenue.

Company executives must choose between options, but the decision should be made after considering the opportunity cost of not obtaining the benefits offered by the option not chosen. For example, difference in costs may arise because of replacement of labour by machinery and difference in costs of two alternative courses of action will be the differential cost. Companies do not record opportunity costs in theaccounting operating expense formula calculator examples with excel template records because they are the costs of not following acertain alternative. Thus, opportunity costs are not transactionsthat occurred but that did not occur. However, opportunity cost isa relevant cost in many decisions because it represents a realsacrifice when one alternative is chosen instead of another. The total cost figures are considered for differential costing and not the cost per unit.

If Bennett worksat the stable, she would still have the tiller, which she couldloan to her parents and friends at no charge. Differential costs do not find a place in the accounting records. These can be determined from the analysis of routine accounting records. All in all, managers often get into situations, where they have to choose from alternatives. Differential Costing is helpful in a comparative evaluation of the substitutes available.

By breaking down mixed costs into their fixed and variable components, businesses can better understand how these costs will change with different levels of activity and make more informed decisions. In forecasting, differential cost analysis helps businesses anticipate future financial performance under different conditions. By modeling various scenarios, such as changes in raw material prices or shifts in consumer demand, companies can better prepare for potential fluctuations. This proactive approach enables businesses to develop contingency plans and adjust their strategies in response to changing market conditions. For example, a company might use differential cost analysis to forecast the impact of a potential tariff on imported goods, allowing it to explore alternative sourcing options and mitigate financial risks.

These could include direct materials, labor, and other relevant costs directly tied to the production. If avoiding these costs saves more money than what is earned from sales, they might stop selling that item. Differential cost, simply put, is the difference in total cost when considering two different options.

By analyzing these costs, companies can determine the most cost-effective production levels and identify opportunities for cost savings through efficiency improvements or bulk purchasing. Understanding the distinction between differential cost and incremental cost is fundamental for effective financial decision-making. While both concepts involve analyzing changes in costs, they are applied in different contexts and serve unique purposes.